2025 Third Quarter Commentary

- Nov 20, 2025

- 10 min read

For a printable version, click here.

If you are a client, click here for a copy of the client commentary which includes discussion of recent investment activity.

Two Things Can Be True At Once

"When people get very excited, as they are today, about artificial intelligence, for example ... every experiment gets funded, every company gets funded. The good ideas and the bad ideas. And investors have a hard time in the middle of this excitement, distinguishing between the good ideas and bad ideas."

– Jeff Bezos at Italian Tech Week, October 2025

“Are we in a phase where investors as a whole are overexcited about AI? In my opinion, yes. Is AI the most important thing to happen in a very long time? My opinion is also yes.”

– Sam Altman, Open AI CEO, August 2025

Artificial Intelligence (AI) is a technology that is decidedly futuristic with many possible applications that have not begun to be contemplated. As a result of the seemingly limitless possibilities, investors have been pouring money into any investment that may drive AI forward. While we have little direct exposure to AI and AI-related investments, the euphoria around these investments now drives the day-to-day stock moves of nearly half the S&P 500. The market is now overvaluing even the most optimistic possible outcomes. Witness Open AI’s recent price to revenue ratio of 38.5 times which is a $500 billion valuation on $13 billion of expected 2025 revenue. That is three times the company’s $157 billion valuation set a year ago in October of 2024. All while Open AI has stated that it expects to burn through $115 billion in cash between 2025 and 2029, an increase of $80 billion (or 328%) from its first quarter 2025 estimated cash burn of $35 billion. These two things can be true: 1) AI is a technology that will likely lead to a more productive future, and 2) many AI and AI-related investments being made today will end poorly due to the high valuations paid for businesses that lack a clear path to profitable returns on the massive amounts of capital deployed.

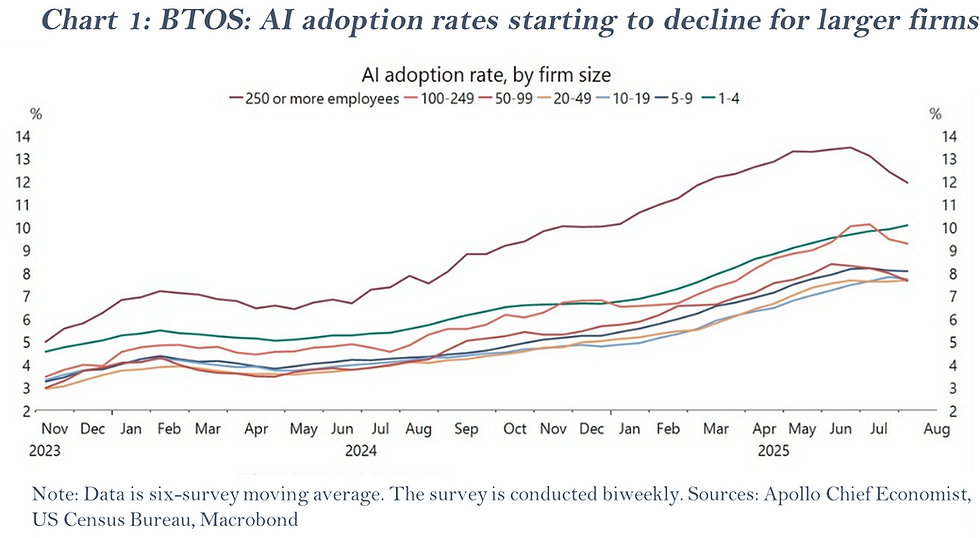

It does appear that AI has positively impacted productivity performance in the U.S. economy. Productivity has grown about 2% annually for two years now, which is a solid improvement on the 1% to 1.5% annual rate that persisted in the decade before 2020. However, according to a recent analysis by Goldman Sachs, most of the increase in productivity has been concentrated in technology, scientific research, engineering and consulting.[1] While rates of AI adoption have been growing rapidly for consumers and businesses, there are hints that the growth of adoption may be slowing. This slowdown is an indication that not all parts of the economy can absorb AI at the same rate. Chart 1 shows the most recent U.S. Census Bureau’s Business Trends and Outlook Survey (BTOS) data indicating a decline in AI adoption by large firms with 250 or more employees.

A widely cited report from NANDA, an AI initiative at the Massachusetts Institute of Technology, provides a clue as to the source of the decline. The report found that 95% of 52 organizations surveyed had a zero return on their AI initiatives.[2]

None of this is surprising, nor is it an argument that AI is not extremely useful in a number of different industries. It is a realistic assessment that new technologies take time to spread and become a part of business processes across the economy. There are all kinds of barriers to adoption, and they have been studied extensively. Software as a service (SaaS) businesses have acknowledged that the product adoption process is an important consideration for user growth for even the best software, and AI adoption will be influenced by it as well. The product adoption process has six stages: awareness, interest, evaluation, trial, activation and adoption. Each stage has points of friction. The uses of AI and AI agents share many similarities to SaaS use cases and are likely to also be subject to the product adoption process. This is not to mention the physical constraints that are present in building the data centers, filling them with processing power and cooling equipment, and securing an extremely reliable and large-scale source of electricity. Any number of these constraints exist when scaling a new business. The worrisome part of the AI euphoria is the amount of money being spent and the speed with which it is being pledged and deployed. The scale and pace have the potential to move far ahead of the hard-to-define probability of generating acceptable returns.

We have seen the AI industry simplified to three big categories: first, there are Foundation and Frontier model companies (Open AI, xAI, Anthropic); second, there are the companies that build tools on top of those models (such as data labeling and data warehousing); and, third, there are applied AI companies building AI agents for various industries and tasks. As AI evolves the industry players continue to become more specialized. We expect the industry will start to consolidate, particularly the Foundation and Frontier model companies. A Foundation model is likely what most of us generally associate with AI. It is a powerful, large-scale artificial intelligence model trained on vast datasets that can be adapted to perform a wide range of downstream tasks with minimal fine-tuning. A Frontier model is the cutting-edge foundation model that is at the forefront of the current capabilities, performing the widest range of tasks with the highest degree of accuracy. Frontier models are considered to be the top-tier of AI models. Frontier models are where vast sums of capital are being spent to develop and try to achieve Artificial General Intelligence (AGI), an advanced version of AI that matches or surpasses human intelligence.

Interestingly, once a Frontier model is surpassed it becomes a Foundational model, and Frontier models are being pushed into the Foundation category at a rapid pace. Recently on the podcast ACQ2 by Acquired, Open AI’s chairman, Bret Thomas, commented, “I’ve heard from multiple investors that foundation models are the fastest deteriorating assets of all time.”[3] When asked what the trainwrecks in AI would be, this sentiment was echoed by former Cisco Systems CEO, John Chambers, in a recent Wall Street Journal interview. Chambers responded, “Train wrecks are going to be companies that are overfunded, spend at a very rapid rate and have little product differentiation in a market which can lose leadership in 12 months. It used to take you five years, and you can lose it in 12 months. The speed of change is huge.”[4] Our takeaway is that the value of the investment in the model you develop is fleeting until you get to AGI. Silicon Valley and tech investors have become enthralled by the prospect of achieving AGI and are convinced it will arrive quickly. Much of these vast sums of money are chasing AGI, which may be like fusion energy, always 15 years away.

The world’s largest technology companies have rapidly increased spending on developing data centers for training and operating AI models. The spending is so massive that the largest spenders have become known as AI hyperscalers. Companies such as Alphabet, Amazon (AWS), Meta, Microsoft and Oracle are spending money on chips, data centers and electrical power at levels that dwarf the largest buildouts in history, including the 19th century railroad boom and the construction of the modern electric grid and fiber-optic networks. These capital expenditures are expected to rise to $347 billion this year from $211 billion in 2024 as seen in Chart 2. Shockingly, as these hyperscaler companies have transitioned from building data centers for cloud services to building AI-centric data centers, the amount spent on data centers as a percentage of operating cash flow has migrated from 30% to around 60%. Frontier AI labs are planning to triple their AI compute capacity over 2024. By 2030, hyperscalers are expected to spend $500 billion per year on AI-related capital expenditures and will need to generate $2 trillion in incremental sales to make a profit on those investments[5], according to a report by Bain & Company.

Chart 3 from the Bain report shows the projection that five years from today hyperscaler revenues will be $800 billion short of the $2 trillion hurdle.[6] And that is with the very optimistic assumption that all on-premises IT will be moved to the cloud by 2030, saving $430 billion a year.

These optimistic projections remind us of the fiber buildout from 1999 to 2003. Back in the late 1990’s, one of the myths that drove the technology boom was the belief that internet traffic was doubling every three months. That belief perpetuated even though it would have meant annual growth rates of more than 1,000%. This led to a rush to install fiber-optic lines to handle all the data movement. Millions of miles of fiber were planned, funded and installed with a “build it and the demand will come” mind set. Decades later, after many of the companies that installed the fiber lines had gone bankrupt, the demand eventually materialized.

Chart 4 shows the growth of fiber supply compared to fiber demand in the early 2000s and the decline of pricing for fiber connections during the same period. An interesting thing to note is that the IT bubble in the stock market burst in March of 2000 and the actual growth in supply of fiber did not really take off until after that point. One of the underappreciated parts of the growth of the internet was the role that the decrease in pricing of fiber played in the eventual growth in demand. We doubt that many of the AI hyperscalers have projected an overbuilding of AI compute capacity and a resulting rapid deterioration in pricing power for their data centers and models. All would argue that they are at the forefront of the Frontier models and will invest to try and stay there, but so far that has proven to be a very expensive endeavor.

The AI bubble today is even bigger by some measures than the IT bubble of the 1990s. Capital expenditures as a share of GDP are much higher for hyperscalers today than for the telecom companies in the late 1990s as shown in Chart 5.

As you can see from Chart 6, the valuation for the top ten today is higher than that of the top ten during the dot-com bubble.

The chart shows 12-months forward price to earnings (P/E) valuations for the top 10 companies (dark green) and then for the S&P 500 Index with (dark blue) and without (light green) those largest index members. As of March 31, 2000, seven of the top ten S&P members were tech and telecom companies. As of September 30, 2025, eight of the top ten were hyperscalers or suppliers to the hyperscalers.

We are Benefitting from AI

We believe that much of the capital being invested to build out AI data centers and develop Frontier AI models will likely have poor returns on investment and therefore we are avoiding investing in those companies. That does not mean our portfolios are not benefiting from the productivity gains that AI is contributing across the economy. Many of our companies are using AI to solve real-world problems. We realize that many of these examples lack the excitement of chasing Artificial General Intelligence, but these are just a few examples of the many tangible ways our portfolio companies are improving their cash flows by leveraging the technology of AI:

Exxon Mobil (NYSE: XOM) – uses AI to process millions of sound waves recorded offshore to map subsea oilfields which has reduced data interpretation time by 75%.

Chevron (NYSE: CVX) – uses AI drones to remotely inspect oilfield facilities for anomalies which reduces drive time for field personnel.

Merck (NYSE: MRK) – uses generative AI to reduce time to produce critical-path clinical study documents from 2-3 weeks to 3-4 days.

Dollar General (NYSE: DG) – uses AI to optimize ordering of its perishable food offerings, reducing inventory “shrink” from expired products.

Comcast (Nasdaq: CMCSA) – uses AI to identify and resolve mass outages on its network, resolving 77% of software issues before customers are impacted.

Kraft Heinz (Nasdaq: KHC) – achieves 12% efficiency gains in pickle production using AI to sort cucumbers by attribute.

LKQ Corp. (Nasdaq: LKQ) – improves quality control and reduces defect rates by using AI to inspect alignment of timing chains and remanufactured engines. (FRM clients can learn more about this recent addition to their portfolios in the Portfolio Updates section below.)

All that Glitters

Despite having limited exposure to the perceived winners in AI, FRM’s portfolios have had a very good 2025 so far. For all the hype over AI this year, gold miners have actually had better performance. This is one part of your portfolio that has contributed to our strong absolute and relative returns so far this year. A gauge of the world’s gold equities from MSCI Inc. has soared about 135% this year, tracking gains in the precious metal, as investors noticed the relentless rally in gold and central banks around the world continued to accumulate the metal. Gold itself has soared more than 45% this year, reaching a series of new all-time highs and on track for its best year since 1979. Newmont Corp. (NYSE: NEM) and Agnico Eagle Mines Ltd. (NYSE: AEM) have seen their New York-listed stocks more than double in 2025 (clients can find more about these two in the Portfolio Updates section below.) Valuations remain reasonable for the gold miners as earnings and free cash flow (FCF) have grown more than the share prices. As Chart 7 shows, the companies in FRM portfolios also have strong balance sheets, having significantly reduced their debt levels over the past decade to now having minimal net debt.

[2] The GenAI Divide: State of AI in Business 2025; https://nanda.media.mit.edu/

[3] ACQ2 by Acquired: How is AI Different Than Other Technology Waves? https://www.acquired.fm/episodes/how-is-ai-different-than-other-technology-waves-with-bret-taylor-and-clay-bavor

[4] https://www.wsj.com/articles/john-chambers-ex-cisco-chief-is-a-vc-now-its-tough-these-days-ee1c8601?mod=itp_wsj

[5] Study assumes a sustainable long-term capital expenditure to sales ratio of 25% for hyperscale cloud providers.

[6] https://www.bain.com/insights/how-can-we-meet-ais-insatiable-demand-for-compute-power-technology-report-2025/

Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Foundation Resource Management, Inc. “FRM”), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from FRM. Please remember to contact FRM if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services or if you would like to impose, add, or modify any reasonable restrictions to our investment advisory services. FRM is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. FRM claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. A copy of FRM’s current disclosure Brochure (Form ADV Part 2A) discussing our advisory services and fees or our GIPS-compliant performance information is available by emailing Abby McKelvy at amckelvy@frmlr.com.

Comments